What is My Federal Income Tax Rate?

Taxable Income

You are not taxed on ALL of your income. There are a number of deductions that can potentially reduce the amount of your income that gets taxed. For most people, the main deduction is what’s called the standard deduction. For 2023, the standard deduction is $13,850 for single filers or $27,700 for married filing jointly.

If your total income for the year is $100,000, only $86,150 is considered taxable income ($100k-$13,850) if you are a single filer.

For most people, taking the standard deduction is the best (and simplest) option, however, if you are self-employed or have significant out-of-pocket medical expenses, it may make sense to itemize your deductions instead of taking the standard deduction. If you think this may be you, talk with a tax professional.

There are some other deductions that can reduce your taxable income. If you contribute to an HSA (Health Savings Plan, not to be confused with an FSA), or traditional IRA (not a Roth) or if you have paid student loan interest fees, this may also reduce your taxable income.

The lower your taxable income, the less you will pay in taxes for the year.

A tax deduction is something that reduces how much of your income is subject to taxes. So if have a $1,000 tax deduction and you are in the 24% tax bracket, it will lower your tax bill by $240.

A tax credit is a direct reduction to the dollar amount you owe in taxes. A $1,000 tax credit will reduce your tax bill by $1,000 regardless of what tax bracket you are in.

Tax deductions and tax credits lower your tax liability (how much you owe).

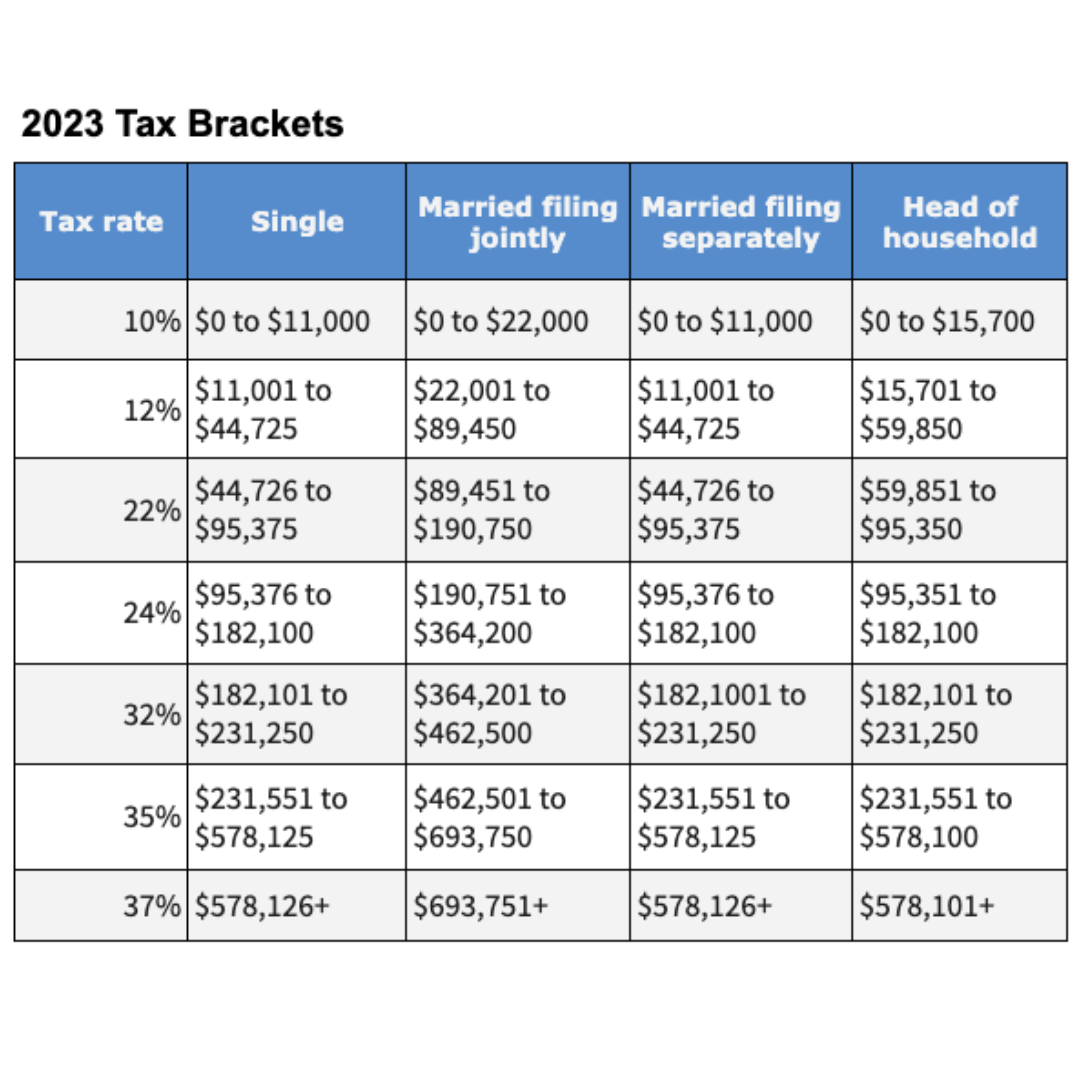

Tax Brackets

In the US, we have a progressive tax system. That means that the more you earn, the higher your tax rate is. Low-income earners pay a smaller percentage of their income to taxes, while high-income earners pay a larger percentage of their income to taxes.

The tax bracket table shows you the range of income at which different tax rates apply.

A common misconception is that whatever tax bracket your total income falls into, is the tax rate for ALL of your income. If, for example, you earn $100k you might assume that puts you in the 24% tax bracket and so you must owe $24,000 ($100,000 x 24% = $24,000) in federal income taxes, right?

In actuality, you are paying the relevant tax rates at each stage of your income.

Let’s say you earn $100,000 (as a single person) and contribute $1,000 to a traditional IRA*.

You’d pay 0% on the first $14,850 (standard deduction + IRA contribution).

You’d pay 10% on the next $11,000 (the amount that falls in the 10% bracket).

You’d pay 12% on the next $33,725 (the amount in the 12% bracket, $44,725-$11,000).

You’d pay 22% on the remaining $40,425 (the amount above the 12% threshold, up until your total income).

In this case, your annual taxes owed is $14,041.

*Most people will have other deductions or credits that apply, but for the sake of demonstrating the math, this example is overly simplified.

Marginal Tax Rate

Your marginal tax rate is the % you pay on your “last dollar of taxable income”. If you are a single filer earning $150k, you are in the 24 tax bracket so your Marginal Tax Rate is 24%. While much of your income is taxed at a lower rate, your “last dollar” or the highest rate that applies to you is 24%.

Effective Tax Rate

While people talk most often about their tax bracket or their marginal tax rate, only a portion of your income is taxed at that rate. Your effective tax rate is determined by dividing the total taxes owed by your total taxable income.

Paycheck Withholdings

You won’t be able to predict exactly how much you will owe in taxes until you know how much you’ve actually earned and what credits or deductions you qualify for. For most people, their income isn’t 100% predictable (maybe they work extra hours, get a raise or bonus, earn interest from a savings account, etc). And sometimes new deductions or credits are announced by the IRS after the year has already started. That makes predicting how much you will owe in taxes a bit of a guessing game.

For this reason, when money is withheld from your paycheck, it’s not based on what you actually owe, but instead, it’s based on an assumption of what you will owe when you file at the end of the year. Depending on how accurate those predictions are, you will either owe money or get a refund when you file taxes the following year.

If your bi-monthly paycheck is $5,000, your employer or payroll company is assuming your annual income will be $120k ($5,000 x 24 pay periods). It’s assuming you will be paid that same amount every pay period, so the amount withheld (sent to the IRS for you) is based on the relevant tax rate for an annual income of $120k.

If however, your paycheck fluctuates a lot and your next paycheck is $7,000 (maybe you worked a few extra shifts), your withholdings for this paycheck will be based on the assumption that you are now making an annual income of $168,000 ($7,000 x 24 pay periods). A large percentage of your paycheck would be withheld from this higher paycheck.

The percentage that is withheld is also based on how you complete your W-4 form (you usually fill this out when starting a new job). The W-4 form allows you to make adjustments to the amount that is withheld from your paycheck.

For example, an employee who is married and has 4 children will have a lower tax rate ( than an employee who is earning the same salary but is single and has no dependents or deductions. Because the first employee will have a lower annuall tax bill, the W-4 form allows them to opt to have less deducted from their paycheck. If they don’t adjust their withholdings (don’t claim any dedpents on their W-4 form) they will overpay their tax bill throughout the year, resulting in a large refund when they file taxes.

If you always get a large refund at the end of the year but would prefer to have less taken out of each paycheck (with a smaller refund), ask your employer how to update your W-4 form.

Bonus Withholdings

Another common misconception is that bonuses are taxed at a higher rate than regular income. When calculating your annual tax obligation (what you owe), bonus income is treated the same as regular income. However, depending on your employers withholding policy, they may withhold a larger percentage of your bonus than they do of your regular paycheck.

If one person has a salary of $120k and their colleague has a salary of $100k with a $20k annual bonus, the amount they will owe for annual federal taxes will be the same. However, the person with the bonus will have more withheld from their paycheck (lower annual take home pay), but will receive a larger tax refund at the year that evens everything out.

Your employer may opt to calculate tax withholdings for bonuses using either the percentage method or the aggregate method.

With the percentage method your employer will withhold your taxes at a flat rate of 22%. Even if you are in the 22% or 24% tax bracket, your marginal tax rate (total taxes divided by total income) is likely lower than 22%, so in this scenario a larger portion of your bonus is infact withheld.

With the aggregate method your employer includes your bonus with your regular paycheck, and your withholding amount is calculated based on the total amount. This payout (including normal paycheck and bonus) is likely higher than your average paycheck, in which case the tax rate applied to the withholdings will also be higher (because the higher the income, the higher the tax rate).

Your bonus, like the rest of your income, is also subject to state income tax (if applicable) and FICA taxes

This blog post is for general educational purposes only. For advise on your specific situation, please reach out to a tax profession such as a Certified Public Accountant (CPA) or an Enrolled Agent (EA).

Our income tax system is complicated, so it’s common to feel overwhelmed navigating your tax obligations. Hiring a professional can help ensure you are not missing out on any tax saving strategies and help alleviate any anxiety related to the process of filing.