Should I Open a Medical FSA?

What is an FSA?

A Flexible Spending Account, or FSA, is an account that helps you save for future medical expenses. With this employer-sponsored benefit, money is taken out of your paycheck, before taxes are deducted, and put into the savings account for you to use on medical expenses. Because you are spending pre-tax dollars, your money stretches further.

Why are FSAs a thing?

Similar to the way that 401ks are an incentive for us to save up for our own retirement, FSAs are an incentive to get us to save for our medical care. Essentially the government is saying they’ll let you skip the income tax on the money you commit to setting aside for medical purposes. By saving for our own future medical expenses (or retirement), we are less reliant on government support.

If people skip routine or preventative care, their health problems tend to get much worse (and cost significantly more to manage in the long run). There are plenty of reasons that people avoid or delay seeking medical treatment. Not knowing how you will pay the bill is a common reason that people avoid going to the doctor. Having an FSA, with money set aside specifically for medical expenses, makes it a bit easier to actually book the appointment.

Who is eligible?

FSAs are an employer-sponsored benefit, so in order to have access to one, you need to be employed by a company that offers an FSA. In 2023, the annual FSA contribution limit is $3,050.

You can use the funds in your FSA for medical expenses for yourself, your spouse, and your children. If your spouse has access to an FSA through their employer, they can also contribute up to the maximum of $3,050 annually.

At the start of the year, you’ll select how much you want to contribute each month, and then you are locked into that contribution rate for the year. If midway through the year you realize that your medical expenses will be more or less than you anticipated, unfortunately, you are not able to change your contribution rate. There is an exception if you have a “qualifying life event”. You are able to make changes to your contribution plan if you get married, have a baby, or you/your spouse starts a new job.

How do you use it?

When you open an FSA account, you will typically receive a debit card connected to your account. You can use this card to pay directly for any FSA-eligible expense. If you are at your doctor’s office and have a co-pay, you pay for it on your FSA debit card. Or if you are at the pharmacy picking up a prescription, or other FSA-eligible items, you may use your FSA debit card to pay for it. Many major retailers (Amazon, Target, Walgreens, etc) indicate which items are FSA eligible, making it easier to identify eligible purchases at checkout.

Alternatively, you can submit medical receipts to your FSA provider and get reimbursed. In this scenario, you’d pay for medical expenses on your regular credit or debit card, then upload a copy of the receipt to your FSA portal. They will then mail you a check for the eligible amount. Note that some FSA plans don’t provide a debit card, so your only option is to submit your receipts.

You’ll want to keep a copy (digital is fine) of all your FSA receipts. In the unlikely scenario that you are audited by the IRS, they may want to see a copy of your FSA receipts. By taking a quick photo of your receipt and saving it in an FSA folder, you’ll save yourself the headache of potentially having to track down an old CVS receipt 3 years from now. When saving receipts, make sure it includes the date of service/purchase, the provider/retailer’s name, description of service or item, your name (or your spouse/child), and the dollar amount paid.

Because there is a little paperwork (or at least scanning of receipts) involved, it is worth considering if the effort is worth the money saved. For many people, the time spent scanning a few receipts is well worth saving a few hundred bucks. But for some, the extra effort may not be worth it.

What is an eligible expense?

Medical expenses that are not covered by your insurance are generally eligible. This includes expenses paid towards your deductible, co-pays, or fees for out-of-network providers.

You can also use your FSA money to purchase medical equipment, baby care essentials, first aid supplies, and many over-the-counter medications. Your FSA provider will have an extensive list of items and services that are covered. Note that some expenses are always covered, some are never covered, and some are covered in certain situations (like if you have a note from your doctor saying this item or service is medically necessary).

The FSA Store has an extensive eligibility list, and you can even order many of the items directly from their website.

Beyond your typical office visit fees, here is a list of common items/services that are FSA-eligible:

Mental health therapy

Band-aids and other first-aid supplies

Tampons and other feminine care products

Nursing supplies, pumps, etc

Chiropractor

Massage - if recommended by a doctor

Glasses and contact lenses

Sunscreen with SPF 15 or higher

What does Tax Deductible mean?

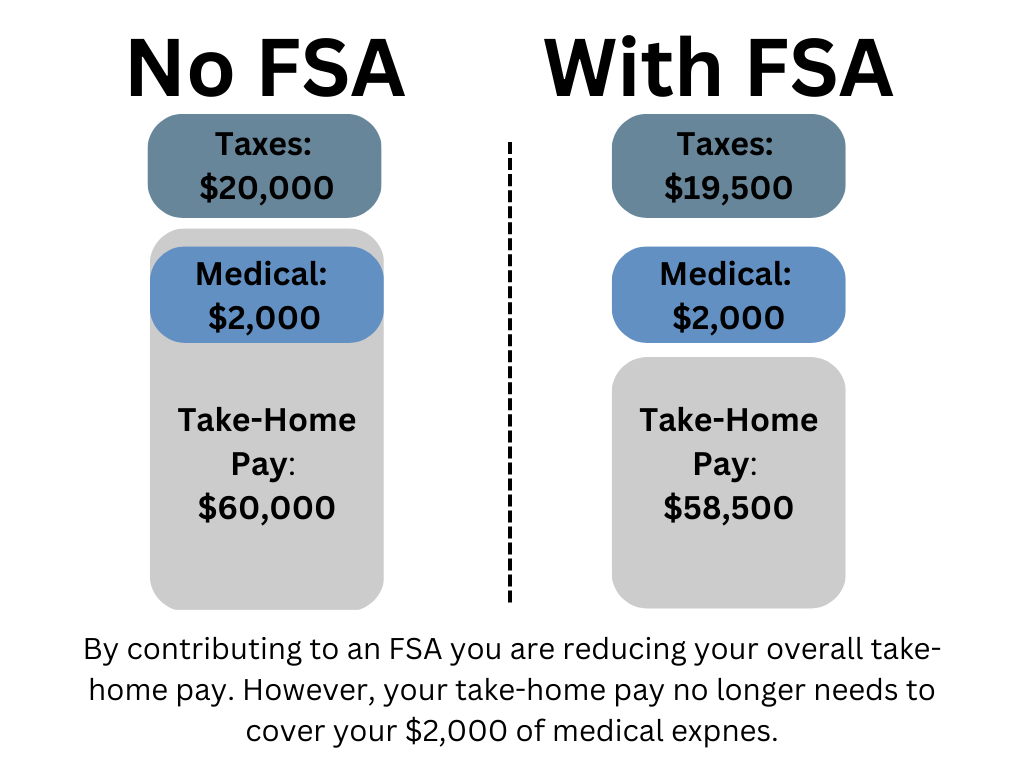

Normally, when we spend money, we are spending after-tax dollars. If you are traditionally employed (someone who receives a W2), your employer deducts your income taxes from your wages before paying you. If you earn a salary of $80,000 a year, about $20,000* of that will is taken out for taxes, leaving you with roughly $60,000 to actually spend, save or invest. In this scenario, you earn $80,000 in pretax dollars or $60,000 in after-tax dollars.

When something is tax-deductible you are paying for it with pre-tax money. If you elect to put $2,000 a year into your FSA, you now only have to pay taxes on $78,000 of income. This means you are paid about $58,500 in after-tax dollars and $2,000 in pretax dollars (to be used for medical expenses). Assuming you have at least $2,000 worth of eligible expenses throughout the year, you now have an extra $500 to spend this year.

Another way to look at is how many working hours it costs you to pay for expenses with aftertax vs pretax money. Let’s say you earn $50 an hour, and have a total of $2,000 in eligible medical expenses. If you are paying for those expenses with pre-tax dollars (through your FSA) it will take you 40 hours to earn that $2,000. If you are paying for it with after-tax dollars (not using an FSA) you will have to earn $2,500 ($500 going to taxes) which will take you 50 hours to earn.

The ability to pay for medical expenses with pre-tax dollars allows your money to stretch further.

While an extra $500 a year isn’t going to make you rich, it’s a nice little bonus for setting aside money to ensure you have the funds available to cover inevitable expenses.

How Much Should I Contribute

FSAs have a use-it-or-lose-it model, meaning you lose any funds you don’t use up by the end of the year. With many plans, there is a limited amount that can be carried over into the next year (as of 2023, employers can allow up to $610 to roll over). But any unused amount, over that rollover limit, is lost.

You want to be thoughtful about how much you contribute. If you contribute more than you will actually use, you may end up losing money (or buying $500 worth of bandaids and pain relievers on December 31st, so your money doesn’t completely go to waste). But if you contribute less than you need, you lose out on the potential tax-saving benefit, and you may ill-prepared to cover unexpected medical expenses.

In order to find the sweet spot, take a look back at your past years' medical expenses. This can help you determine a baseline for your typical medical expenses. If you have ongoing prescription costs, frequent office visits fees or copays, or you regularly see an out-of-network provider (therapist, chiropractor, acupuncturist, etc) it makes sense to contribute enough to your FSA to cover (at least most) of these expenses.

While we never really know what is in store for us in the future, sometimes we can anticipate when our medical costs will be going up. If you are expecting a child or plan to seek new medical treatment, you can assume your costs will be higher than usual and may want to contribute more to an FSA.

Understanding what your insurance policy does, or does not, cover can help you better anticipate your out-of-pocket costs. With many policies, your will be paying in full for most services until you reach your deductible. This means you may have a lot of out-of-pocket expenses early in the year until your deductible is hit, but then very few costs from then on. Contributing enough to your FSA to at least cover your deductible can help smooth out your cash flow by covering those irregular expenses.

It can also be helpful to scan the list of eligible expenses to see which items you regularly purchase already.

No one is going to hit the exact right number, so don’t stress out about getting it perfectly. Aim for a number that at least covers your regular routine medical costs. If your company allows for a rollover, you may opt for a slightly higher number, knowing there is a buffer if you don’t use all of it by the end of the year. If this is your first year using an FSA, it can make sense to start conservatively. Pick a number you know you will likely hit. Then next year you will have a better idea if that's a number you should stick with, or if you want to increase your contributions.

Childcare FSA

This article is focused on Medical FSAs, but there are also FSAs specifically for childcare costs. It works similarly, in that you elect to have pre-tax money deducted and put into an account. Then, as you probably assumed, those funds can be used to cover childcare costs. For parents with kids in daycare, afterschool care, or summer camps, this is a great way to stretch your money a little further.

HSA

An HSA, Health Savings Account, is a tax-deductible account that is used for eligible medical expenses, similar to an FSA, however, an HSA is only available to people who are insured on a High Deductible Health Plan (HDHP). While the HSA has a lot of similarities to an FSA, there are a few key differences.

While an FSA is only available through your employer, and HSA is available to anyone with an HDHP. So if you are self-employed, you can open an HSA, so long as you are on a high-deductible insurance plan.

Unlike an FSA, where you have a limited amount of time to use the money you’ve contributed, with an HSA you can use the funds at any point in the future. So you don’t have to worry about contributing more than you actually needed for the year.

Lastly, most HSAs have the option to invest a certain amount of your balance in the stock market. The money invested in an HSA is triple tax-advantaged (a topic for a future blog post), so if you have the ability to put extra funds into one, it can be a great option for long-term/retirement investing.

If you know that you’ll have medical expenses next year, an FSA is a great way to proactively save for them while also saving on your income taxes.

*Calculations based on a 25% marginal tax rate. Your actual tax rate will depend on your income, your spouse's income if applicable, and your state income tax rate if applicable.