Planning for the Cost of Christmas

The end of the year is notoriously expensive, particularly if you celebrate Christmas.

If you love the holiday season, it's easy to get swept up in the magic of it all and spend a small fortune in the process. And, if you aren’t a Christmas fanatic, you may end up feeling a little bitter about how much it costs just to avoid looking like a total Grinch.

For many people, overspending at Christmastime feels almost inevitable. It’s common to just close your eyes, swipe the card, and wait for January to see how much damage you’ve done to the credit card.

I’m not advocating for completely rejecting all forms of the commercialization of Christmas. However, being more mindful of the expenses you take on, and actively creating a plan ahead of time can ensure that the holidays don’t prevent you from achieving other financial goals. And, it can help you avoid that spending hangover come January.

Setting Realistic Expectations

I often hear people telling themselves they “aren’t going to go overboard this year”. Recognizing that you don’t want a repeat of last year’s overspending is great, but to change your behavior, you need to create an actual plan of how you will spend less.

Creating some specific spending boundaries for yourself makes it easier to avoid overspending. That might look like:

I’m only buying gifts for the people on my list.

I won’t spend more than $50 on new decorations this year.

I’m not going to look at any of those Holiday Gift Guides, because they always cause me to buy things I don’t need.

I will unsubscribe from any retailer’s promotional emails

I won’t buy anything on Black Friday unless that specific item was already on my list

Another challenge is that we often don’t recognize all the added costs associated with the Christmas season. While gifts are the main expense that we usually think of, often many other holiday expenses sneak in.

Common holiday/year-end expenses that we forget to factor in:

Christmas tree and new holiday home decor

Traveling to see family

Attending numerous social events or festive outings

New outfit for the office party

Hiring a photographer for your annual family Christmas card

All the extra little treats you indulge in because “‘tis the season”

Charity donations

Year-End appreciation gifts (ie Teacher, Housekeeper, Mail Carrier, etc)

These expenses are easy to overlook, and they are often harder to say no to, even if your bank account balance feels dangerously low. With these seasonally specific activities, the FOMO factor is particularly high. And if you have young kids, the internalized pressure to make the season feel magical can be intense.

To be clear, there is no shame in doing all of these things. If you enjoy going all out for Christmas, fantastic, just recognize and plan for the cost. However, if you don’t particularly enjoy these activities, and are just doing them out of societal expectation, you may want to be more selective in which holiday traditions you choose to participate in.

Planning for this year

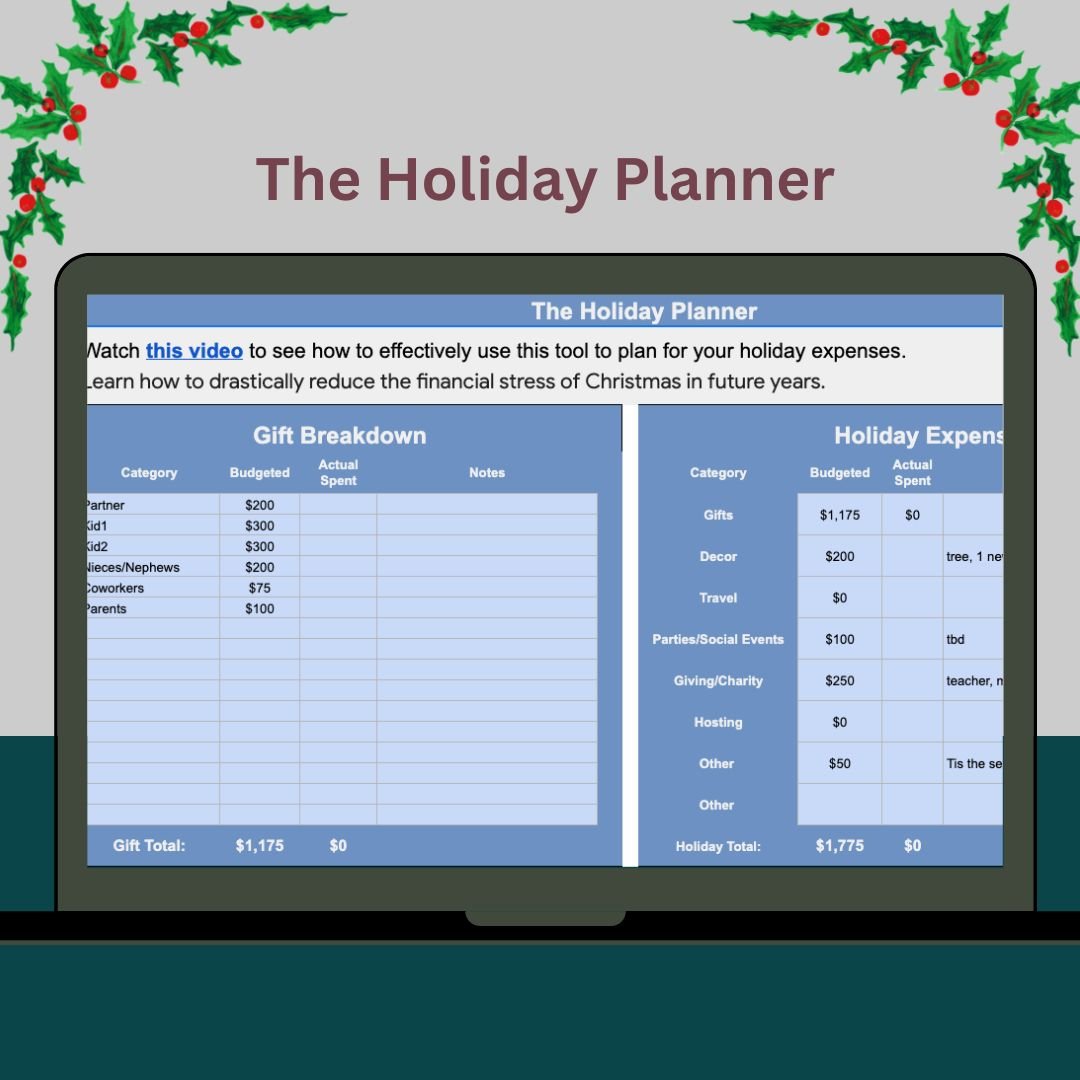

As we head into the Christmas season, it’s a great time to start thinking intentionally about a Christmas budget. The Holiday Planner is a helpful tool for you to map out your expected expenses.

The Holiday Planner - a tool to help you anticipate and plan for your holiday expenses

Gift Planning

Start by writing out a list of everyone you plan to give a gift to, including a rough dollar amount of what you plan to spend for each person.

By mapping out who you plan to buy gifts for, and estimating the total cost, you’ll have a good sense of how much gift-giving is going to set you back.

If the estimated cost is more than you can comfortably afford, now is the time to evaluate if you want to reduce how much you will spend per person, or consider if there is anyone you can remove from the list. Presumably, everyone on your list cares about you, and wouldn’t want you making significant financial sacrifices just to give them a gift.

With a plan in place, it’s a bit easier to avoid impulse purchases. We’ve all come across something too cute not to buy, so we think of someone we could buy it for, just to have an excuse to buy it. Yes, I’m sure your co-worker's baby will look adorable in that festive onesie, but by having a clear list of who you’ve budgeted to buy gifts for, hopefully, you’ll pause for a moment to consider if adding more people to your list last minute is really a priority for you.

Planning for Non-Gift Expenses

Next, you’ll want to identify all the other related holiday expenses. Try to be as realistic as possible. You might not need any new holiday decor, but if you are self-aware enough to know that you can’t make it out of a Target without some new festive items, you might want to build it in.

Are you traveling to see family over the holidays? Flights and hotel costs are the obvious big-ticket expenses, but if you need to rent a car, get gas, or extra meals out, be sure to factor those in too.

Or are you hosting at your house? Hosting a big meal usually means a spike in grocery and alcohol costs. If you are having people stay with you, will there be any extra expenses to get the house “guest friendly”, like a new set of sheets or a new air mattress?

It’s common for people to give Christmas or year-end gifts to people like teachers, childcare providers, housekeepers, or mail carriers. If you haven’t incorporated that into your budget it can put you in an uncomfortable position of having to choose between being generous (and possibly overextending yourself) or sticking to your budget (but feeling stingy). So if you have anyone in your life that you want to give to, plan for it.

Similarly, people often give more to charities at this time of year. It can be hard to be as generous when your bank account is feeling uncomfortably low (or your credit card balance is scarily high). So if giving to charities is part of your year-end plan, add it to The Holiday Planner.

Are you prone to self-gifting? While scouring for the perfect gift for your loved ones, you might feel the urge to treat yourself to a gift as well. If this is a common scenario, you may want to build that into your budget, too. Or, if your holiday spending already feels like more than you can actually afford, this is a good time to set some limits for yourself.

The primary goal of this exercise is not necessarily to reduce your costs (although it might help with that), but to recognize and anticipate the costs. That’s not to say you need to stick to your plan with 100% accuracy. Having a plan that you MOSTLY stick to, is still going to serve you much better than not having a plan at all.

Covering the Costs

Once you have an idea of what the holiday season is going to cost you, you need to create a plan for how you will actually pay for it. Depending on how far in advance you are planning, you may have time to start setting aside money so you have a little reserve going into December.

If you haven’t saved up ahead of time, and the projected holiday spending total is more than you can squeeze into your regular monthly budget, you will likely need to either dip into savings or put the extra expenses on a credit card. If you are putting expenses on a credit card that you won’t be able to pay off right away, it’s important to consider how the credit card interest fees change the total cost of Christmas.

For example, let’s say you put $2,000 worth of Christmas expenses on a credit card with a 29.99% interest rate, and make monthly payments of $200. You will be making payments until December of the following year, and you’ll have paid an extra $330 in interest fees.

Putting Christmas expenses on a credit card, to be dealt with later is a reality for many people. Just make sure you have a plan for how you will actually pay the balance off.

Planning for Next Year

After you’ve projected your spending for this year, I recommend tracking what you actually spend. If you go over what you budgeted, don’t beat yourself up. Instead, make a note of how you feel about all the different purchases.

What are you glad you spent the money on?

In hindsight, what could you have skipped?

Are there any things or experiences you wish you’d spent more money on?

Taking some time to reflect on what brought you and your loved ones the most joy will make it easier to make a better plan for next year.

Now that you know what you spent on Christmas this year, and have some insight on an ideal Christmas budget for next year, you can start saving up well in advance. If you take that goal amount and divide by 12, that’s how much you need to put away each month to ensure you’ll have enough saved up in December.

For example, if your goal is the have $2,400 available to spend guilt-free next year, you can open a savings account and set up an automatic transfer of $200 per month, starting in January. By splitting up the payments into 12 installments, it will ensure that you have $2,400 available to spend by next December. So you won't need to cut out other expenses, dip into savings, or put purchases onto a credit card.

Get your free copy of The Holiday Planner so you can feel more confident that you are spending on the things that matter most to you, and that you aren’t spending more than you can afford.