What should I do with my Tax Refund?

Getting a tax refund is a great problem to have. However, deciding what to do with it can feel overwhelming. Should you do something responsible with it? Or is this your opportunity to splurge on something exciting?

When deciding what to do with this extra cash, some helpful questions to ask yourself are:

What priorities are you struggling to fund with your regular income?

How can this money be most impactful?

If saving for a big financial goal feels impossible to squeeze into your monthly budget, this may be a great chance to jump-start that goal.

Or, if you are managing to chip away at those bigger, responsible, goals, but never feel like there is enough left over for you to spend on the fun stuff, maybe this refund is a good way to build in a budget for the vacation or the wardrobe upgrade you’ve been coveting.

Reflecting on how it can best impact your life can help prevent impulsive purchases that only offer a brief dopamine hit. And while it’s great to make a plan for how you will use the money once you get it, avoid pre-spending it. Wait until you actually have the money in your account before you start using it.

You also want to avoid overspending or over-allocating your refund. With a refund on the horizon, people often justify numerous purchases, only to realize the cost of their extra spending is higher than their refund.

Payoff high-interest debt

Paying down debt may not be the most fun way to use your refund, but it can be a huge boost to your overall financial picture. Having high-interest debt (ie credit cards, payday loans, etc) can cost you a lot in interest fees. If you are only making the minimum payment, it might take you a long time to pay off your balance. Using your refund to make a larger lump sum payment now can have a significant impact on your debt payoff timeline, and help you avoid some of the interest fees.

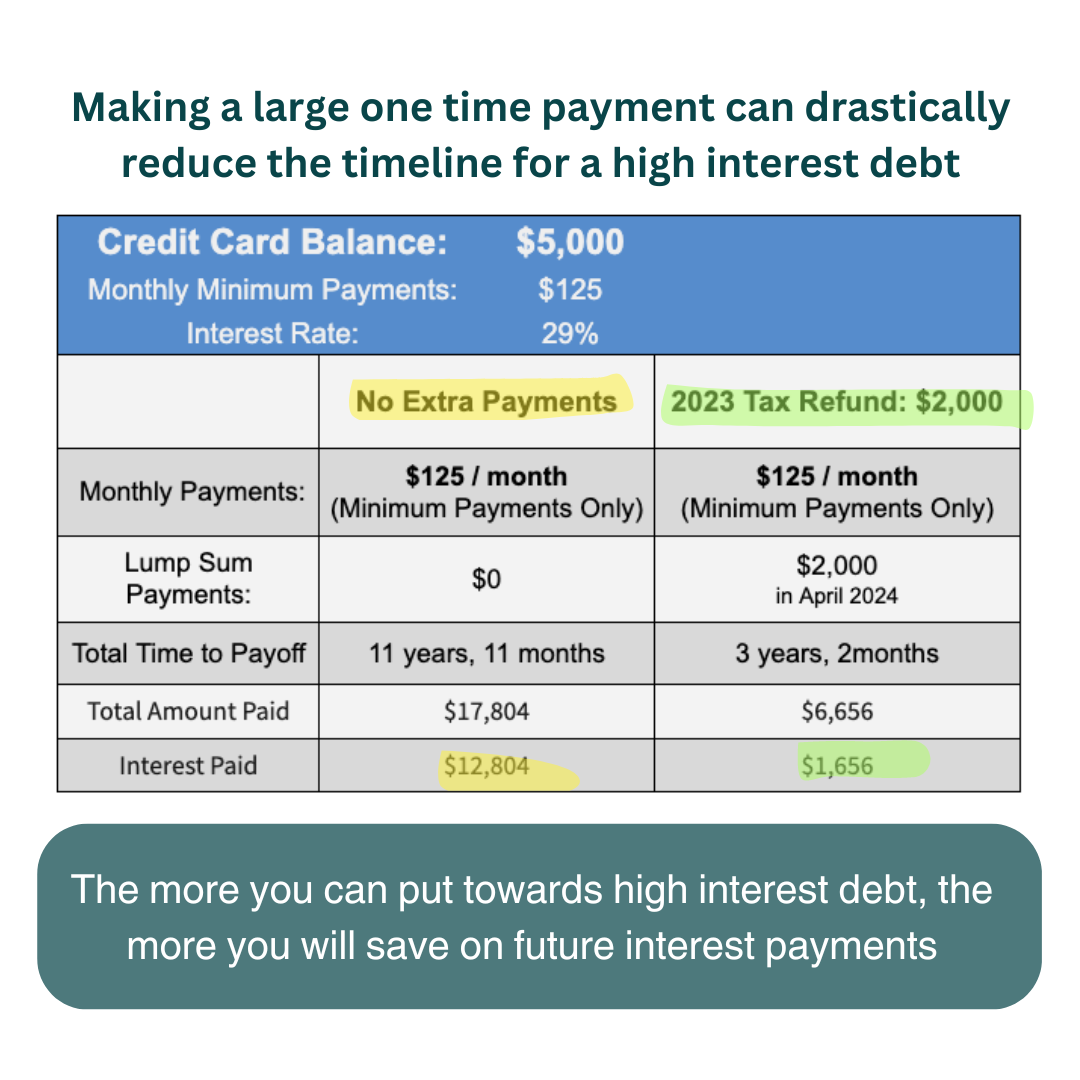

Let’s say you have a credit card with a $5,000 balance that has a 29% interest rate and a $125 monthly minimum payment. If you continue just making the minimum payments, it’s going to take you almost 12 years to pay off the balance, and you will have paid $12,804 in interest fees over that time.

Alternatively, if you have a $2,000 tax refund and you put all of it towards your credit card balance now, then continue with your monthly $125 payment, that drops the payoff timeline down to 3 years and 2 months. Your total interest fees paid in that time drop to $1,656. By putting your $2,000 refund towards your high-interest debt, you’d save yourself over $11,000 in future interest fees.

Comparison of credit card payoff options

Build your Emergency Fund

Having money set aside in a separate account, that is earmarked to be used when an emergency expense pops up, or to help fund your life in the event of a job loss, is a great way to protect your future self from financial catastrophe. While saving for future catastrophes isn’t the most fun use of your money, saving for those unpredictable, but inevitable, expenses is a very responsible choice.

The standard recommendation is to set aside 3-6 months’ expenses in an Emergency Fund. While that is a fantastic goal to shoot for, it can feel so daunting when you are first getting started, that for some people it doesn’t even feel worth it to try.

By putting your tax refund into an Emergency Fund you can make a big leap towards your goal (even if you are still a ways off from that 3-6 month target). Once you have a decent base in your Emergency Fund, it feels less overwhelming to continue adding small increments to it each month.

Short-term savings goals (Sinking Fund/Savings Bucket)

A savings bucket is an account that you have earmarked for a specific purpose or goal.

Typically, you would add a little bit to this account each month, but if you have a tax refund coming, that’s an easy way to expedite the timeline for these short to medium-term goals.

Common sinking fund uses include:

Future house down payment

Home repairs/renovation

Car repairs/new car purchase

Travel

Pet expenses

Retirement Investing

If you are feeling a bit behind on your retirement investing (or if you’ve already managed to check off the boxes of your other savings/debt payoff goals), putting a large chunk of money towards your retirement investments is a fantastic use of a tax refund.

Because of the magic of compound interest (your money’s ability to grow over time), even a small amount put into a retirement account now can grow significantly by the time you are ready to retire.

Spend it

If you are already making progress towards your other financial goals, or if there is an urgent expense (i.e. necessary car or home repairs, medical bills, etc), choosing to spend your tax refund money right away may be part of an overall financially responsible plan.

However, if you’ve got high-interest debt, don’t have much in savings, or haven’t managed to put much away for retirement, you may want to consider the impact of choosing to spend the money now, instead of prioritizing those other goals.

Split it up

If you are feeling the urge to splurge, allocating a portion of your refund to spend on a fun indulgence can be a good way to satisfy the desire, without sabotaging your ability to move your financial life forward.

Consider adjusting your withholdings

If you consistently get a large tax refund every year, you might consider adjusting your tax withholdings. By having less money withheld from each paycheck (less taken out for taxes), you’ll have the ability to save/invest/spend more each month. A large refund typically means that you were giving the government more than you needed to from each paycheck.

Sometimes people opt for a higher tax refund (choosing to have more withheld than necessary) because it is the only way they know how to make themselves save. If they get a little more each paycheck, they may not trust themselves to use it wisely.

While it’s not inherently wrong to opt for the larger withholding/larger tax refund option, allowing the government to hold onto your money can cost you. You may have heard that getting a larger refund is “giving a tax-free loan to the government”. If you have high-interest debt, having your surplus tax withholdings held by the government (instead of you taking it and using it to pay down debt) means you will incur more interest fees than necessary. Alternatively, if you take those surplus tax withholdings and put them into a high-yield savings account or an investment account, your money could be growing throughout the year.

Learning to make better day-to-day spending decisions is a skill that can be developed. If you don’t trust yourself to make good financial decisions when you have access to more money, you might benefit from some outside support. Working with a 1:1 financial coach will speed up the learning curve on your journey to being financially savvy.